How to Pay for College

Figuring out how to pay for college is a very common concern among prospective college students and their parents.

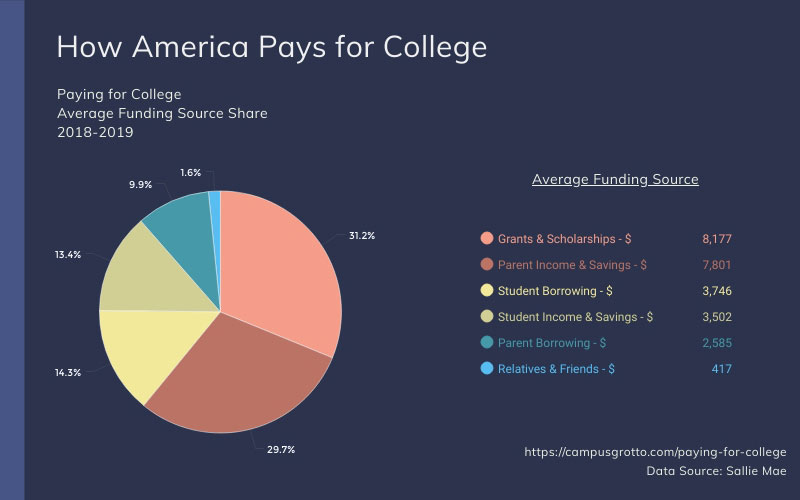

Most college students pay for college using a variety of resources. No matter which college financing alternative you choose, you should still complete the FAFSA (Free Application for Federal Student Aid) as well as any financial aid forms required by your school.

Here we'll take a look at some of the various ways of paying for college and how you can get financial aid to help with the cost of going to college.

Applying for Financial Aid

The majority of students going to college receive some form of financial aid, whether it is student loans, scholarships, grants, or even work-study. These funds are essential for most students as it is the only way for them to complete their college education.

In order to obtain these funds, every student must fill out the FAFSA (Free Application for Federal Student Aid). This form must be filled out every year the student attends college, if they wish to receive aid.

While financial aid forms may seem overwhelming at first, use these FAFSA tips and resources to have a better understanding of the process to get financial aid and properly complete your application.

FAFSA Deadlines

The FAFSA deadline is one of those dates that can sneak up on you and is here before you know it. Mark your calendars. This is surely a deadline you won’t want to miss, as you don't want to be left out of any possible financial aid disbursement.

The Federal FAFSA deadline is June 30. However, the deadline for your state or school may be different than the Federal deadline and additional forms may need to be completed. Check with a financial aid administrator at your school about state and school sources of financial aid and deadlines.

When you submit your FAFSA on the web, be sure to take note of the confirmation page and store it for your records as this page has a confirmation number with the exact date and time the form was received and is your proof that you filed on time.

If you miss the deadline, you can still submit your application, just be sure to work with your school’s financial aid office to ensure that your request is reviewed for any remaining funds.

Federal Student Aid ID

A FSA ID is required to access certain U.S. Department of Education websites and to electronically sign your FAFSA form.

Documents Needed for FAFSA

In order to fill out the FAFSA you will need specific documents to ensure that you complete your application accurately. Use the checklist below to determine if you have all of the necessary materials to proceed with your application:

- W2 and/or Tax Forms - If you are a dependent student, you will need copies of this information from your parents. If you are an independent student, you can use your own tax information. If you are married, be prepared to enter your spouse’s information. It is best to complete your tax return BEFORE filing your FAFSA; this will ensure you receive the correct amount of funds for the current year.

- Other Income - If you receive other income besides your employment, such as unemployment, Social Security, child support, etc., then be prepared to enter these amounts.

- Bank Statements - One of the questions on the FAFSA will ask you what the current account balance is in your bank account, so you should be prepared by having your most recent bank statement handy.

- SSN and Drivers License Number - If you do not have your Social Security number and driver’s license number memorized, then have these documents ready as well.

- Assets - If you have any other assets or investments, you will need to know the current value of them so have these documents ready for reference.

- Non US Citizens: If you are not a U.S. Citizen, you will need to make sure you have your permanent resident ID Card.

Finally, check with your school for additional financial aid forms that may be required. Some schools will require a separate form and may also need additional financial information to determine if you are eligible for any kind of state aid or funds available from the school.

Any other questions about the application can be answered at the FAFSA Frequently Asked Questions page.

Ways of Paying for College

Student Loans

Most students turn to some type of student loans for college to cover the cost of going to college. You can use these college loans not only for tuition, but for books and other educational-related expenses as well.

How to get Student Loans

A big worry among prospective students is whether or not they will be able to afford college.

If you are a student faced with a situation of trying to get a student loan, you are not alone. The process itself is fairly easy and the benefits, of course, are the ability to have the money needed to pay for college and get a degree.

Luckily, a student loan is one of the easiest loans to obtain. All you usually need is a cosigner and you can be approved for a decent size student loan to use on your college expenses.

The good thing about student loans is you typically don't have to start paying them back until after you finish school. Of course, when trying to get financial aid for help in paying for college, you should always try and get grants and scholarships first, as those don't have to be paid back. Check out scholarships for college and see what you can qualify for. It may not seem like it, but an extra $1000-$2000 towards your college education can really come in handy.

Federal Student Loans

The government offers subsidized and unsubsidized student loans that can be obtained by filling out the FAFSA. Subsidized loans are for those who demonstrate financial need and the interest on the loan is paid by the government while you're enrolled.

The basic eligibility requirements for a Federal Student Loan are:

- Show financial need.

- Have a valid Social Security number.

- be a U.S. citizen or an eligible noncitizen.

- Be studying for an eligible degree or program.

- Maintain satisfactory academic progress.

- Not be in default on a federal student loan.

- Register for the Selective Service (if you are a male and between the ages of 18 and 25).

If, for some reason, you are not eligible for a federal student loan, you can always go with a private student loan. Many private lenders can offer financing for college and these loans can still qualify for student loan consolidation.

Private Student Loans

Private student loans are issued based on your credit and that of a cosigner. The better the credit score, the lower the interest rate.

Typically, students just graduating from high school don’t really have an established credit record, making it hard for them to get a loan by themselves and if they do, it generally is at a very high interest rate. This is where a cosigner comes in handy.

Having a cosigner with a decent credit score will get you the best interest rate possible. This is a huge bonus because the difference between a 5% and 10% interest rate is huge in the long run and can save you thousands of dollars over the lifetime of the loan. Also, having a cosigner will allow you to apply for premium student loans and increase your chances of being approved.

It seems like a no-brainer to use a cosigner on a private student loan. The real question is how does cosigning for a loan affect the cosigner? One must know that cosigning for a loan means the cosigner is guaranteeing to repay the loan should the borrower fail to make the required payments.

One of the best candidates to cosign are parents since they will usually help out with college costs and will probably be the easiest to get to cosign.

Here are some steps to take when looking for student loans:

- You usually need a good co-signer, so keep one in mind.

- Talk with your school's financial aid counselor.

- Fill out the FAFSA and get it in on time. Check FAFSA deadlines.

- Check with your bank.

- Check local credit unions.

- Ask relatives, maybe they can help fund your education.

- Check out student lenders online.

Most Common Types of Student Loans

- Stafford Loan: Stafford loans are available to most students regardless of income and credit history. They are either subsidized or unsubsidized depending on your financial need, which is determined by the government. If your Stafford Loan is subsidized, then the U.S. Department of Education will pay any interest that accrues on your loan while you are in school or while the loan is in deferment. If your loan is unsubsidized, then you, as a student, are responsible for the interest. These are not need-based loans, however there are borrowing limitations depending on your enrollment status and class (freshman, sophomore, etc.).

More info about Stafford Loans

A Stafford Loan is a student loan that is offered to eligible students in order to help finance their college education. The loan itself is described in detail in Title IV of the Higher Education Act of 1965 that guarantees full payment to a lender if the student does not satisfy the terms. The loan offers rates that are much better than private student loans since the US Government guarantees them in full.

With that said, these loans do have very strict eligibility requirements that needs to be met before any money is given out. Students applying for these types of loans must first fill out the FAFSA. The Stafford Loan is available directly through the FDSLP (Federal Direct Student Loan Program) or from a private lender through the Federal Family Education Loan Program. (FFELP).

Students receiving these types of loans are not required to pay off the loan until they cease to be a full or half time student in college. After the student leaves school, either by graduation or by not fulfilling the minimum credit requirements, a 6 month grace period kicks in. After that 6-month period, the loan repayment process begins.

Stafford Loans are available both as subsidized and unsubsidized loans. The difference being that subsidized loans are technically interest free for the time you are in college and for the 6 month grace period as the federal government will pay those recurring interest rates for the student. On the other hand, unsubsidized loans have interest added to the total amount even while you are still in college.

- PLUS Loan: If you are a dependent student, your parents can apply for a Federal PLUS Loan to cover the expenses of your college education. PLUS loans are credit based, therefore your parents should have a good credit history in order to be approved for these types of loans.

More info about Parent PLUS Loans

There are many various ways of paying for college available to students to assist with the cost of college. There are times, however, when you exhaust all of your resources and still need money to cover your college tuition. If you are a dependent undergraduate student, then your parents can apply for a PLUS Loan to help you pay for educational expenses, such as tuition, room and board, and books.

What is a PLUS Loan?

A PLUS loan is one that your parents or legal guardian can apply for to assist you with your educational expenses. Parent PLUS loans can usually cover the gap between other federal student loans and grants. A credit check is performed for PLUS loans, however they are a little easier to obtain than traditional private student loans. The amount that can be borrowed is equal to the amount of tuition minus all other loans and grants received.

Do you need to fill out the FAFSA?

Yes and No. The FAFSA, Free Application For Federal Student Aid, does not have to be filled out to be considered for a PLUS loan, however, a lot of schools will still require the FAFSA as part of your financial aid package and may not verify the PLUS loan without a FAFSA in your financial aid file.

Where does the money come from?

The money for Parent PLUS loans either comes from private lenders under the Federal Family Education Loan Program (FFELP) or the funds may come from the government under the William D. Ford Direct Loan Program. Some states may act as a guarantor under the FFELP program, making it easier for parents to obtain the loan. This means that if your parent defaults on the loan, the state that is guaranteeing the loan will pay the funds back to the lender, and then your parent will have to pay the guarantor.

Other Parent PLUS Loan Information

- Since these loans are federally guaranteed, the interest rates are usually pretty low, but still carry a higher rate than a Stafford Loan.

- PLUS loans are not based on need. There is a credit check, though not as stringent as private banks, making it easier for most parents to obtain the loan.

- Parent PLUS Loan repayment traditionally started about sixty days after disbursement, however as of July 1, 2008, parents have the option of deferring payments on PLUS loans until after graduation. Interest will accrue on the loans during deferral, but the deferment helps by providing more flexibility in the repayment of the loan.

- If your parent is not approved for a PLUS loan due to negative credit, they can apply with a co-signer, or you can resort to other financial aid options, such as private student loans.

- Unlike some private loans offered through banks, PLUS loans do not require any type of collateral.

- There is no income requirement for a PLUS loan, which makes it easy for most parents to obtain the funds needed so that their child can continue their education.

- PLUS loans can be consolidated. If your parent has PLUS loans out for other children, they can consolidate student loans and possibly lower their payments.

- The interest may be tax deductible. Have your parent talk to their accounting professional when filing their taxes.

Remember, a PLUS loan is not free money. It is a loan and has to be paid back. If your parent does not pay back the loan, it will have a negative impact on their credit history.

- Private Student Loans: Private student loans can also be used to supplement federal student loans when federal loans, grants and work-study are not enough to cover the cost of education. Private loans for college can be obtained from any bank or credit union. Being a credit-based loan, it is wise to apply with a co-signer if you do not meet the income and credit requirements. Private student loans may be used for any education-related expenses such as tuition, room and board, books, computers, and more.

While using student loans for college is one of the common methods of paying for college, students should understand that it is not their only option when it comes to paying for their college education.

College Scholarships

College scholarships are great because it provides free money for college that doesn't have to be paid back. There are many types of scholarships out there: Academic Scholarships, Need-Based (Financial) Scholarships, Sports Scholarships, clubs or member-based scholarships, and more.

Where to Find Scholarships

Students can apply for scholarships through companies, states, or even through their own college.

There are a few great scholarship search websites out there that have huge databases of scholarships, so it may be worth your time to check out these resources.

Some scholarship applications may be time consuming, requiring a written essay, or something similar, so make sure you qualify for all the requirements and follow college scholarship tips.

Since most scholarship sites require you to enter personal information, it's important to find a site you can trust. You don't want them selling your info or trying to scam you. For instance, many scam scholarship sites ask for a "fee". This should never be the case and if you see this, stay away from the site.

When looking for scholarships, check out these websites that offer an extensive list of current scholarships.

These are some of the best scholarships websites out there:

- FastWeb

The cool thing about FastWeb is that their scholarship search results are personalized. When a new user signs up, they fill out a personalized questionnaire about themselves which is used as the basis for the scholarship results they provide. Scholarships are broken down by scholarship type, college, internship, job, need based, academic and more. This will save you time by not displaying the scholarships you may not be eligible for. FastWeb is the best scholarship site out there and it is highly recommended to check them out and hopefully get your hands on some free money for college. - College Board

The College Board scholarship search website may have a lengthy questionnaire, but you have to remember that the more information you can provide for these scholarship search tools, the more detailed and targeted scholarships they can find for you. Though time consuming, filling out the required information will save you time in the long run, as you go down your list of eligible scholarships. - Scholarships.com

Registering here can gain you access to 3.7 million scholarships and grants worth over $19 billion. They have both local and national college scholarships on file. You can also receive notifications and updates on new scholarships and upcoming deadlines. - StudentScholarshipSearch.com

This website does not require registration to browse or search scholarships. Scholarships are conveniently divided into respective categories.

All these sites have great access to huge databases of scholarships. The leader in the industry and best scholarship search site by far is FastWeb.

10 Tips on How to get a College Scholarship

These Ten Tips will help you in getting scholarships to pay for college:

- Start ASAP and Apply Early - Many scholarships have early application deadlines, so don't miss out on these opportunities.

- Search Locally - A local scholarship is probably your best chance for getting a college scholarship. There are special scholarships just for locals, meaning it will be less competitive, as there are usually less applicants. Local banks, grocery stores, clubs, businesses, organizations, and churches are all potential sources for community scholarships. Also check State-funded scholarships. States have lots of money to disperse when it comes to providing education.

- Read the Requirements - Make sure you are eligible right from the start, so you’re not wasting your time. Also, never pay to apply for a scholarship, these are usually scams.

- Follow Instructions Carefully - Any errors right off the bat can get your scholarship application easily denied. Proofread it. Have someone else proofread it.

- Neatly Presentable, Neatly Packaged - Send the scholarship application via certified mail or better yet, FedEx, making your application look professional and stand out from others.

- Communicate - Make sure the application is right. If you are not sure about something in the scholarship application, don't hesitate to ask.

- Check School Specific Scholarships - Check with the college you would like to attend. Usually there are many school-specific scholarships available. This alone may be able to help you in your school decision making.

- Visit a financial counselor at your School - A financial counselor may be able to lead you to scholarships you don't know about or that aren't listed on the web. Find scholarships that aren't very competitive by applying for ones that are not heavily advertised.

- Be Active, Stay Active - Being in a sports team, club or some type of community service will always better your chances at receiving a college scholarship.

- Maintain your GPA - Keep your grades up. A higher GPA will make you eligible for more scholarships, on top of increasing your chances of receiving funds.

Bonus: Download the book, "Confessions of a Scholarship Winner: The Secrets That Helped Me Win $500,000 in Free Money for College - How You Can Too!" for free on Amazon.

College Grants

Educational grants are funds that are allocated to students that meet the requirements of the giver. Some schools are given money by donors to use for their grant program. The federal government provides a Pell Grant to financially-needy undergraduate students. Grants do not have to be repaid.

Federal Pell Grant

The Federal Pell Grant is a post-secondary education federal grant program sponsored by the U.S. Department of Education. These types of grants are awarded based on a financial need formula that is determined by the U.S. Congress via the FAFSA application.

One of the great benefits of a Federal Pell Grant is that the funds do not need to be repaid. They are usually awarded to undergraduate students who have not earned a bachelor’s or any other type of professional degree. In this sense, a Pell Grant is considered as federal financial aid and additional aid from other sources, either federal or non-federal, may be added on top.

The maximum Pell Grant award for the 2022-2023 year is $6,895. The amount available usually changes every year depending on the funds that the program has available. The maximum that an individual can get depends solely on the individual’s financial need, their cost to attend school, and their status as a full-time or part-time student.

Federal Pell Grants are usually applied toward tuition costs but arrangements can be made to pay the student directly (most likely via check). During limited occasions, a combination of these methods might be used. As far as regulations for the school, they must tell you in writing how much your award will be and the method that you will receive payment. Additionally, schools must disburse funds at least once per term.

Work-Study

Work-Study is when a student is given a part-time job (usually on campus) and the earnings from the job are allocated to pay for the student’s tuition. These jobs are usually awarded to financially-needy students first, and then to other students if any jobs remain available.

As previously stated, you must fill out the FAFSA to be eligible for Stafford Loans, Work-Study, grants and even some scholarships. Check with your school for additional paperwork regarding any of these alternative resources, as well as a complete list of scholarships available.

Federal Work-Study Program

Have you ever wondered how your friend got that part-time job working as a clerk in the admissions office or how your classmate scored a cool job stocking textbooks at the school bookstore? Well they may have received those jobs as part of a Federal Work-Study Program.

What is Work-Study?

Federal Work-Study is a program where a student can work part time to earn money, which will be applied towards the tuition balance at their school. These assignments are usually awarded to students who exhibit financial need. Need is determined by the school by using a formula created by the government.

How does it work?

Since the government funds Federal Work-Study, the minimum hourly wage is equal to or greater than the federal minimum wage. Students usually work a minimum of about 10-15 hours per week with the maximum being 20 hours. Jobs can be located on or even off campus at federally-approved companies, however the job at off-campus facilities must be in the best interest of the public, such as non-profit organizations or community facilities.

How to Apply for Work-Study

In order to apply for Work-Study a student must fill out the FAFSA. When filling out the FAFSA, there will be a section which will ask which types of financial aid you are interested in, such as loans, grants and work-study. Be sure to check this box, as this will alert your school(s) that you are interested in this program as part of your financial aid package.

Work-Study Benefits

There are quite a few advantages of the Work-Study program. First, since this is a federal program, you can be guaranteed that your part-time hours are flexible enough to revolve around your school schedule. Also, when you fill out your FAFSA the following year, the money you earned through work-study is not counted as income to determine your need for financial aid. Finally, the best part is that you get to work and the money is automatically applied to your outstanding tuition balance. If you combine Work-Study with student loans, grants, and college scholarships, paying for college becomes much easier and less stressful.

Other Work-Study Tips

Every college and university that participates in the work-study program has their own preset rules and terms regarding the process. If you are awarded work-study as part of your financial aid package, make sure you ask some questions so that you get the most out of your experience. You should be sure to ask questions such as: “Do I have to find a job or will one be assigned to me?” or “What will my hours be?” You also want to be sure that when you are finally assigned your job that you show up as scheduled.

Other Options for Paying for College

- GI Bill - A popular benefit provided by the military.

- 529 Plan - Long-term college saving plan that offers tax and financial aid benefits.

- Student Loan Consolidation - When it comes to paying for college expenses after graduation, some borrowers may want to consider consolidating their student loans into one payment.

Paying for College Resources and Websites

Useful websites to help with paying for college from our student resources page: